STORIES

Designing an alternative account for millennials

October, 2016 | BY Claudia A. Baron & Caryn Englander

Recently, Global Marketing partner Caryn Englander sat down with Claudia A. Baron, from Mastercard’s Global Prepaid Product Development to talk about creating a new account product for Millennial cardholders.

Caryn Englander: Why are you developing a product for Millennials?

Claudia Baron: We have all seen the data—one third of millennials are willing to switch banks within 90 days, more than 50% don’t think their bank offers anything different than other banks, aand more than 75% are more receptive to Apple, Google, or Amazon to provide financial services than to traditional banks. We believed these trends have nothing to do with liking or disliking banks, but pointed to an expectation gap. Millennials are looking for whatever they need to be delivered digitally, immediately, and all in one place. Banking is no different.

CE: Where did you begin the process?

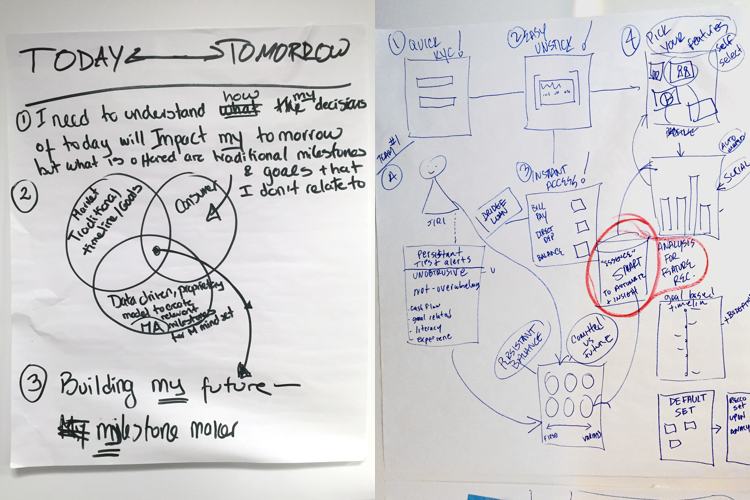

CB: We started with the consumer segmentation work done by the Marketing Insights team, and focused on young working singles and couples, or “pre-nesters” to get a sense of who they were, what motivated them, and how they spent time and money. With that as a jumping off point, we conducted workshops with cross-functional teams to further explore the needs, tensions, and expectations that working singles and couples are negotiating. For example, the tension between being indulgent and being responsible, being spontaneous and being a planner, and the tension between how a person behaves individually vs. the way they behave in a relationship. The workshops helped us identify ways we could help negotiate these tensions within targeted experiences. We identified three distinct value proposition territories we could pursue. The first was around simple money management, the second was around shared money management, and the third was around socially responsible banking.

CE: What do you mean by targeted experiences?

CB: Targeted experiences are the moments where there are functional and emotional needs that we can use to anchor our focus and explore different solutions.

CB: We used sketching techniques to bring to life, explore, and evaluate what a potential solution looked like. For example, we explored ways in which we could alleviate the friction around something like simple money management. These sketches were a free form of ideation and had no boundaries. They gave the groups freedom to stretch their thinking and crystalize how we could diminish the tension in the given situations.

CE: Where did you end up?

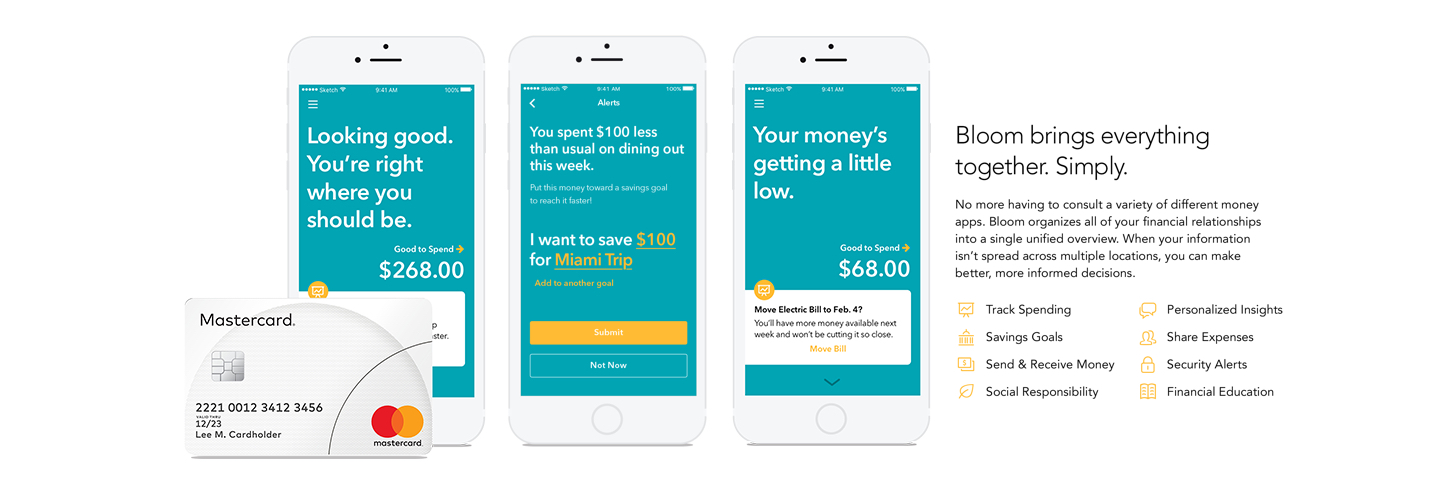

CB: We ended up with a product we are currently calling Bloom. Bloom is an alternative digital bank account that includes a mobile app and a payment card that allows you to securely receive, manage, send, and spend your money. It consolidates and simplifies money management activities into one easy-to-access service. We arrived here because we understood that this target needed to do all their financial activities in one place. When you think about how Millennials manage money, they have four to six apps in their phone that help them do so. They may have Venmo, their bank app, Mint and more. The problem they have is making sense of all these disjointed experiences to get at the heart of truly understanding where they stand financially.

CE: How do you know consumers will think Bloom solves their needs?

TCB: We created a clickable prototype to bring the concept to life and to help us further test our solution with consumers. The prototype took us around three weeks to develop and proved to be a critical asset in helping us prioritize, validate and refine the concept with consumers in both qualitative and quantitative research.

The prototype also helped us validate and begin selling the concept with our multiple distribution partners (banks, MNOs, and retailers).

For our qualitative study, we conducted two weeks of online testing with students, working singles, and working couples in three markets. This study helped us confirm our understanding of their needs, identify which value propositions were most appealing to them, and gain additional insights on how to refine the concept and the kinds of services we will need to provide. Then we conducted a quantitative study in eight markets to validate the refined concept and understand the services needed to deliver our “most lovable product” for launch. Next, we will test again in a controlled pilot with our target segment.

"We want a product that will exceed consumer expectations, and will grow with them as they go through their financial journey.”"

CE: I’ve never heard the term “most loveable product” before. What do you mean?

CB: It’s the bar our team has set for ourselves, because “minimum viable product” is not acceptable to us. We want a product that will exceed consumer expectations, and will grow with them as they go through their financial journey. We believe between the assets Mastercard already has, and those that we can integrate from the right partnerships, we will deliver a valuable product in a way that makes our digital solution more loveable than others out there.

CE: That sounds very promising. Will you keep us posted on your success?

CB: Of course. But it isn’t just our success. It will be a success for all of Mastercard, because the platform that enables Bloom will be useable for the development of other products in the future.

Claudia A. Baron

Claudia is the Global Solution Design and Consumer Experience Lead for Global Prepaid Product Development. She works with Prepaid Global teams and the Regions to identify consumer opportunity areas based on insights and needs, design differentiated solutions and drive end-to-end product and service experiences.

Caryn Englander

Caryn is the Global Product Marketing partner supporting prepaid and debit. She works with product management and development in identifying consumer targets and needs, product positioning, and the articulation of why Mastercard products and services are a better choice.