STORIES

Co-creating a digital credit experience with consumers

JULY 2016 | BY NICOLE OW

Standard Credit is our entry level product, and is targeted at "pre-nesters" (working singles and working couples) who are new to credit. Since the product itself is entry-level, it has all of the great Mastercard benefits like zero-liability, a line of credit, emergency services, and access to brand assets like our Priceless programs, but none of the bells and whistles of a product for more affluent customers.

The question we wanted to answer was, what was going to make Standard Credit appeal to pre-nesters? We believed the answer was the way in which they experienced the product. Our hypothesis was that if we could find a way to deliver seamless and intuitive digital account access, this would resonate with pre-nesters.

We developed a strong concept based on consumer insights and tested it in communities of consumers. They loved the features related to virtual cards and budgeting, and that helped them feel in control of their finances. Features like this were not new to the market; therefore, how theseemergency services features were delivered was going to be the most important part of the product we eventually developed. And who better to tell us how to design these features than the target consumers themselves?

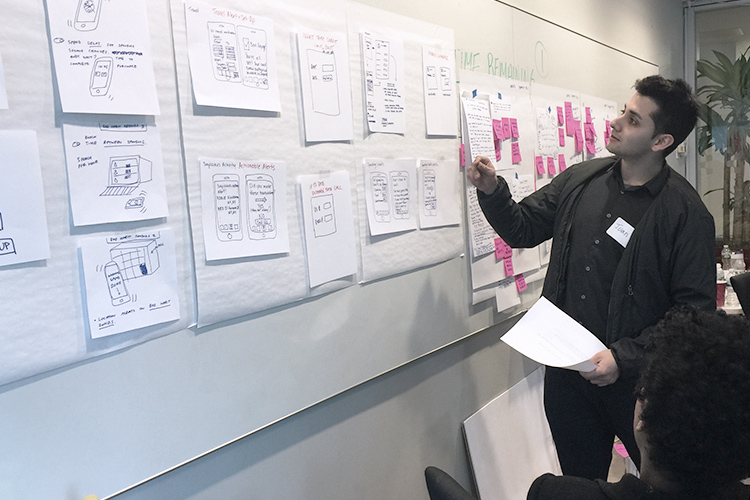

We decided to do a consumer co-creation workshop with 18 pre-nesters to hear directly from them what they wanted in a credit card and how they wanted to interact with and manage it.

In March 2016, a cross-functional team from Mastercard, including Credit Product Management, Product Development, Marketing, and our partner Sapient came together with 18 pre-nesters to really flesh out some of these ideas. The one-day session was held in NYC and facilitated by a team at Sapient. We came up with scenarios before the session and asked pre-nesters to sketch out on paper what that experience would look like if they were to design it themselves.

We had very engaging discussions and learned a lot from our prospective consumers. The good news for us was that we were on the right track with our product— they validated features we had already identified as important. We also learned that this group wanted everything to be quick and visual: think colorful images and as little text as possible. This was just one of the insights we gathered that day that informed the overall design of the experience.

We also got some very original ideas from the session. One participant came up with a feature that would allow a cardholder to set budget limits, and when they exceeded the budget it would post embarrassing pictures to the cardholder's social feed with no explanation. This feature wasn't something we pursued, but the important insight it provided to us was that pre-nesters wanted their financial money management to be fun.

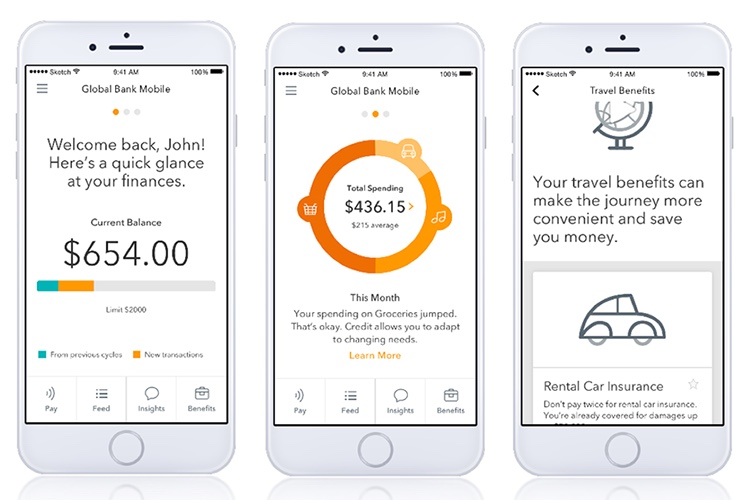

The next step in the design journey was to take all of this great input and develop a prototype. We left that day with hundreds of new ideas for features or enhancements to features we had already thought of that we could incorporate into the prototype. All of the features were ranked against feasibility, consumer value, and business value. There were passionate discussions about what features needed to make the cut— it was tough because so many of the ideas were so great. Eventually, we agreed upon a list of features that aligned with our agreed-upon value proposition. Finally, we built the prototype over a four-week period, made up of weekly sprints, that focused on different elements of the prototype.

At the end of the design phase of the project, we had a clickable prototype that we could share with internal partners and card issuers to help bring our vision to life. The quality of the discussion became so much richer when both parties could really visualize what we meant when we talked about the ideal end-to-end consumer experience.

There is a lot more work to be done. We need to test this prototype with more consumers to see if we got it right, and what features may need a bit more work and refinement. But, we can do this in an agile and iterative way to get to a place where we truly have delivered what our consumers asked us for. This prototype is a great first step in delivering an experience that is designed with the consumer at the heart of it. After all, we designed it with their ideas that we gathered from our co-creation sessions with them.

NICOLE OW

Nicole is Mastercard's Global Consumer Experience Lead for Consumer Credit. She works with regional and other global teams to improve the experience of Mastercard's consumer credit products for cardholders.